The essentials of the Forschungszulage

.png)

Forschungszulage – The Essentials at a Glance

The Forschungszulage is a central instrument for tax incentives supporting research and development (R&D) in Germany. It is intended to encourage companies of all sizes and industries to invest in innovative projects and drive innovation forward. Eligible costs include personnel expenses for R&D employees as well as costs for contract research and assets.

The program has been available since 2020 and is gaining importance through continuous adjustments. Exciting new changes will also come into effect in 2026. In this article, we provide a comprehensive overview of how the Forschungszulage works, who can use it, and the advantages it offers.

.png)

What Is the Forschungszulage?

The Forschungszulage is a tax-based R&D incentive regulated by the Forschungszulagengesetz (FZulG). It can be claimed by companies in Germany that conduct research and development activities.

The special feature: the funding is not provided as a grant that must be applied for and approved in advance, but as a tax credit via the tax return. This means that even companies without profits benefit, since in this case the allowance is paid out by the tax office as a refund.

The Forschungszulage is industry-independent – what matters is not the sector in which a company operates, but whether the projects meet the legally defined R&D criteria. You can learn what these criteria are and how they are assessed in our article Forschungszulage – Criteria & Requirements at a Glance.

Who Can Apply?

The Forschungszulage is open to all companies subject to taxation in Germany – regardless of legal form, size, or age. Eligible applicants include:

- Sole proprietors, freelancers, small businesses

- Partnerships (GbR, OHG, KG)

- Corporations

- Collaborative projects and contract research

There are no minimum size or turnover requirements. Start-ups and small businesses can also benefit, as long as they carry out eligible R&D projects. Contributions made by sole proprietors themselves are also eligible.

Excluded: Companies in acute financial difficulties, such as those in ongoing insolvency proceedings or with unstable financing situations.

Eligible Activities

The law distinguishes three types of eligible projects:

- Basic research – experimental or theoretical work aimed at gaining new knowledge without direct commercial application.

- Industrial research – targeted research to develop new products, processes, or services.

- Experimental development – systematic work to develop new or significantly improve existing products, processes, or services.

Key features of a project include novelty, the presence of technical or scientific uncertainties, and a systematic, planned approach. More on the specific criteria & requirements can be found here.

Amount of Funding

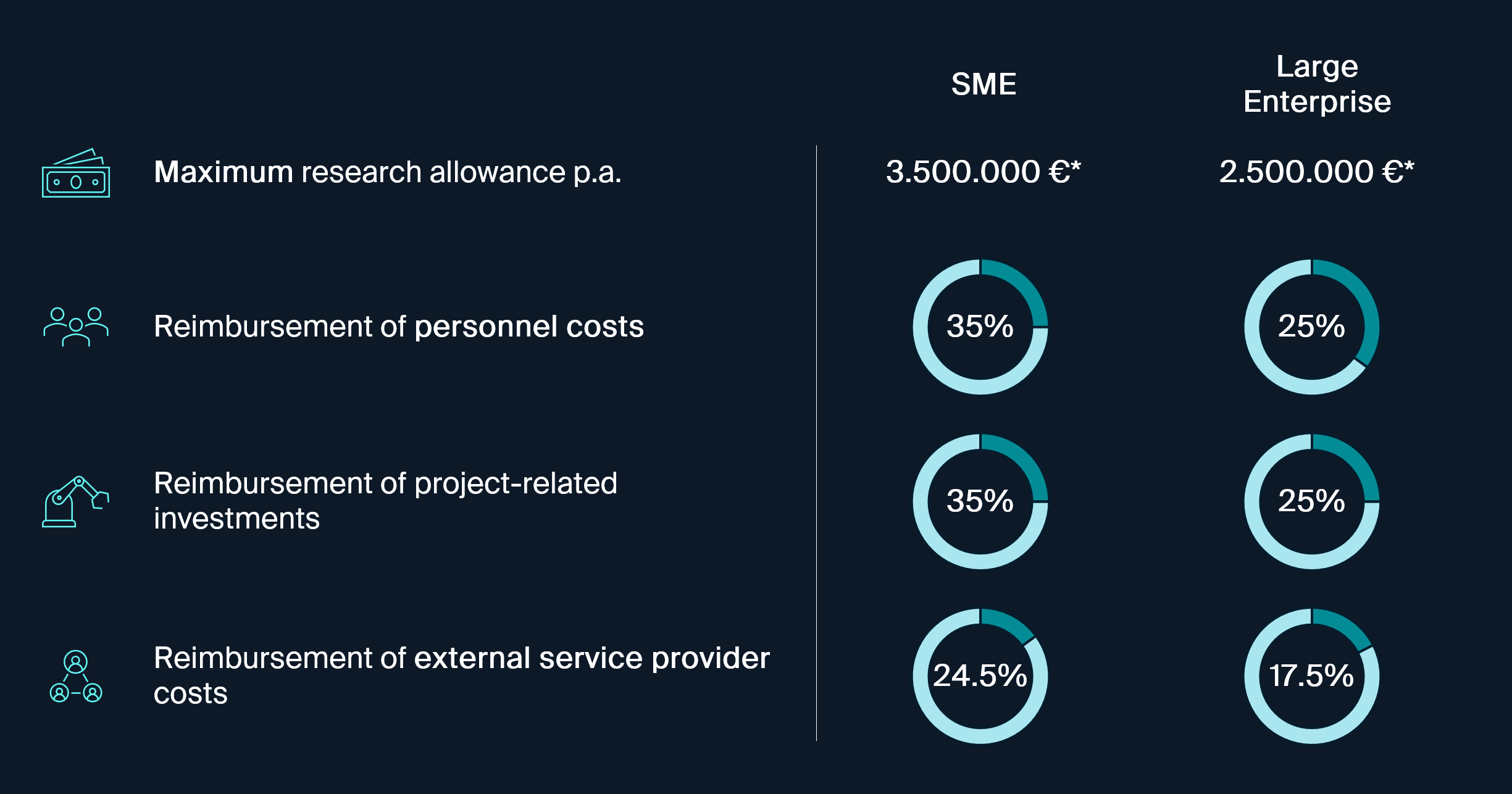

The Forschungszulage is calculated based on the eligible expenses for approved R&D projects. For in-house projects, this primarily includes personnel costs for employees directly involved, including employer contributions to social security. Depreciation on movable fixed assets used in R&D can also be taken into account. The eligible base amounts to up to €10 million of qualifying expenses per fiscal year.

The current government coalition has announced plans to expand the Forschungszulage – including higher funding rates, a broader base, and a simplified application process. More on this in our article Forschungszulage 2026: Higher Funding & New Rules.

Application Process

Applying for the Forschungszulage involves two steps:

- Technical review by the BSFZ (Bescheinigungsstelle Forschungszulage):

First, the process begins with an online application for a BSFZ certificate. The BSFZ reviews only the content-related eligibility of the project, not the financial details. - Tax application via the tax office:

Once the BSFZ certificate is available, the Forschungszulage can be claimed in the company’s tax return. The tax office verifies the stated costs and processes the payout after completing the assessment.

Advantages of the Forschungszulage

The Forschungszulage offers companies several concrete advantages:

- Planning security – the criteria are legally defined, so with the right project selection and documentation, there is a clear legal entitlement.

- Liquidity effect – even companies without profits benefit, as the allowance is paid out as a tax refund.

- Open to all industries – any company with eligible projects can apply.

- Combinability – the Forschungszulage can be combined with other funding programs, provided costs are not funded twice.

Legal Basis

The Forschungszulage is based on the Forschungszulagengesetz (FZulG), which came into effect on January 1, 2020. The interpretation of the criteria follows the OECD Frascati Manual, the international standard for defining research and development.

Deadlines & Timing

.png)

- The Forschungszulage can be applied for retroactively for up to four years – even for completed projects.

- The BSFZ application can be submitted at any time – before, during, or after a project.

- The tax claim is filed with the tax return once the certificate is available.

Requirements for a Successful Application

- Knowledge of the necessary criteria and requirements

- Familiarity with the application process

- Complete and transparent project documentation

More Funding. Less Effort.

The Forschungszulage is an effective funding instrument, accessible to a wide range of companies. It provides clear legal conditions, can be combined with other programs, and generates positive liquidity effects – even in loss-making years.

With proven expertise and established processes, DnA Ventures ensures that your Forschungszulage is approved quickly. From the first consultation to securing your funding, we provide the support you need.

Curious how much funding your R&D projects could receive?

Let’s find out!

.png)

Related

topics.

Explore additional articles on the Forschungszulage to deepen your understanding of eligibility, application strategy, and funding updates.

.jpeg)

.png)